Fundamental analysis answers the question of why the price moves, but not the question of when to enter, and a trader needs exactly the second answer. The market responds not to the report's figure itself but to its divergence from expectations, and large capital manages to play that out before the news reaches retail. So I keep macro as a background and the direction of the wind, while the entry itself I take by volume and the price's reaction at a level.

I make a point of not trading the news and don't build forecasts from the calendar; my lens is the chart, volume and levels. I've traded this way for years. But know the background I must, and every week I mark in my reviews what's coming out: Fed meetings, inflation, employment. All of it breeds volatility, and often it's right at key levels that the market turns, and that's already my territory. This guide brings the whole fundamental side together: what moves the markets, how to read the data and why retail is almost always late on it.

In this article we'll cover:

- fundamental analysis answers why the price moves, but not when to enter, and for timing it's weak;

- the market is moved not by the fact itself but by its surprise relative to expectations, while large capital positions ahead;

- the market moves most sharply on central-bank rate decisions, with inflation, employment, GDP, PMI and geopolitics alongside;

- at the moment a release comes out I don't enter; I read the market's reaction and the footprint of large capital by volume at a level.

Let's start with what fundamental analysis even is and why a trader needs it.

What fundamental analysis is and why a trader needs it

Fundamental analysis is a method of valuing an asset through the study of economic and financial factors: central-bank rates, inflation, company reporting and the state of the industry. Its goal is to determine the fair value and compare it with the market price: cheaper than fair, the asset is considered undervalued, more expensive, overvalued.

Over a long horizon it's a strong approach, the very one on which Warren Buffett built a fortune, holding quality companies for years, and I honestly acknowledge its power over a span of years. But a trader lives on a different scale of time: what matters to them is not where the asset will be in five years, but where it will go in the coming hours and days. This is exactly where fundamentals stall, because they explain the cause of a move, not its moment. I'm no opponent of this tool, I just understood long ago that the question of when to enter it doesn't close, and that's precisely the one a trader needs. So my position on fundamentals I lay out in detail in the course section on fundamental analysis, and below I'll lay out how it all works: the factors, the indicators, the rates, the calendar and what I watch instead of the news.

In short: Fundamentals value the fair price through the economy, rates and reporting; for an investor like Buffett it's a strength, but to a trader it says why the price moves, not when to enter.

Which economic factors move the financial markets

The list of driving forces is no secret, and it's worth keeping the whole of it in front of you. The cost of money in the economy is set by the central-bank rate. The pace at which life gets dearer is shown by inflation. The economy's health is signalled by employment, and in the States its main gauge is the monthly report on new jobs outside the farm sector. The balance of exports and imports is summed up by the trade balance, and a firm surplus as a rule props up the currency. The mood of business is measured by PMI, where the dividing mark sits at 50. Commodities, gold and geopolitics stand apart.

Gold is a special case here, it's a safe-haven asset. When the world gains more uncertainty and fear, investors flee from risk into protection, and demand for gold jumps; on geopolitical flare-ups this is seen best of all, when the risk sentiment turns capital flows around. These flows move largely on the crowd's emotions, on its fear and greed. One thing matters: all these factors create a background and volatility, but on their own they don't tell a trader in which second to enter.

In short: Markets are moved by central-bank rates, inflation, employment, the trade balance, PMI, commodities and geopolitics; gold meanwhile stands apart as protection, and demand for it flares up on fear.

The main macroeconomic indicators: GDP, PMI, inflation, employment

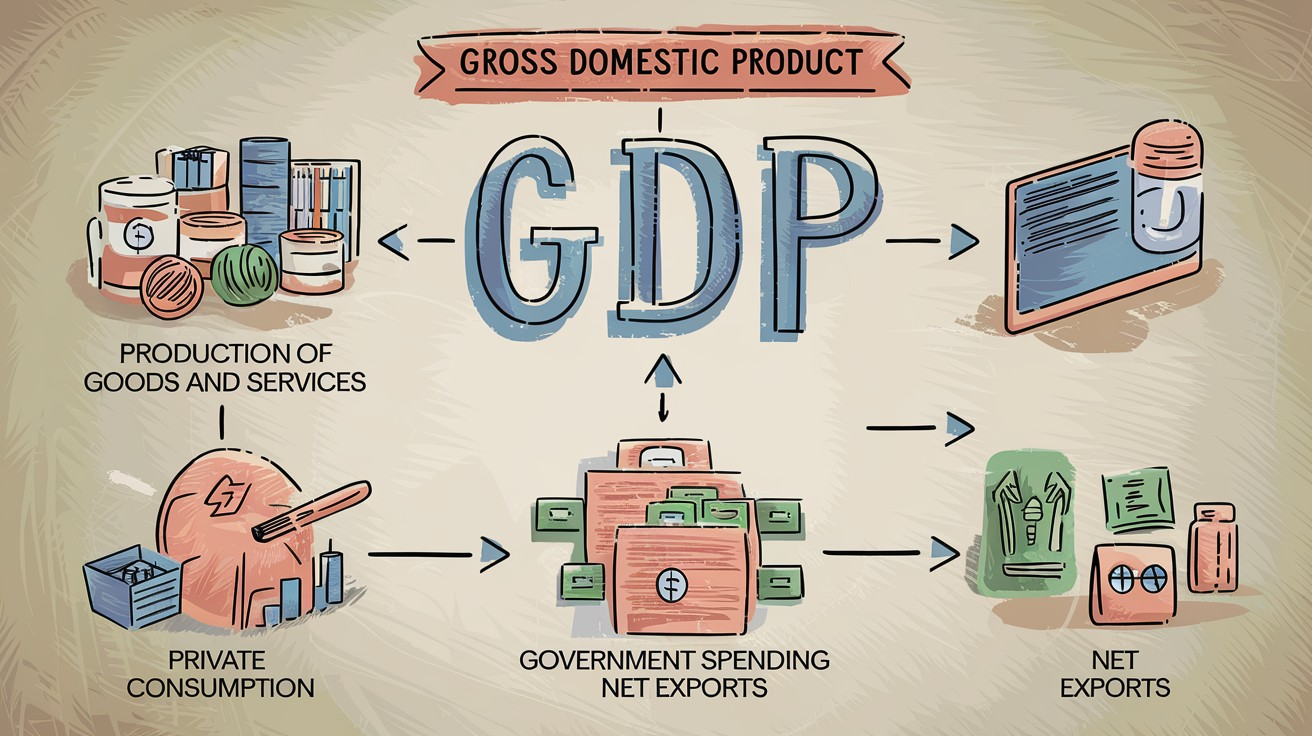

GDP is the total value of all the goods and services a country has produced over a period, and the main gauge of the economy's size and growth. GDP grows, the economy firms up and the appetite for risk is higher; it falls two quarters in a row, and talk of a recession begins. But as a trader I treat it evenly: it's a lagging indicator, it describes what has already passed, and large capital has usually played it all out by the time of publication. So GDP for me is a background, not an entry signal.

Alongside stands PMI, a barometer of business activity from surveys of purchasing managers, with the same pivotal mark of 50: above it the economy expands, below it contracts. Unlike GDP it's leading, the mood of business turns earlier, so the market reacts to PMI more keenly than to belated figures. Inflation is measured by the consumer price index, and it's critical in that the central bank looks at it when deciding the rate's fate. Employment completes the picture: a strong labour market supports the currency, and the US jobs report sharply jolts the dollar. And here's the key thought for a trader, worth grasping at once: the market is rocked not by the fact itself but by the surprise, that is the deviation of the figure from expectations. Even a brisk report drops the price if the market expected brisker still. These data I've gathered deeper into a review for general horizon, but beginners I'd advise not to bury themselves in the calendar, but first to learn to read the chart.

In short: GDP lags, PMI leads with a 50 boundary, inflation and employment rule the rate; but the market is moved by the gap with expectations, not the fact, so at the data release itself I don't enter.

The key rate and the Fed: how central-bank decisions move the dollar and assets

The key rate is the percentage at which the central bank lends to commercial banks, the main lever for managing the cost of money in the economy. The logic is simple: they raise the rate, money gets dearer, the economy slows, inflation is reined in, the currency usually firms up, and risk assets like stocks and crypto get a tighter squeeze. They cut the rate, it's all the other way: money gets cheaper, the dollar weakens, and stocks, crypto and gold get support. It's important to remember the lag: between the decision and the economy's real response there usually pass more than six months, so the trends caused by the rate stretch out for a long time.

The main player here is the Fed — the Federal Reserve System, the central bank of the United States, which manages monetary policy through the rate and the quantity of money in the economy. The dollar is the world's main currency, so the Fed's decisions echo across the whole planet. But the Fed isn't alone, and the difference in the banks' policies is exactly what moves currency pairs. The ECB answers for the euro and is usually more cautious than the American regulator. The most curious example is the Bank of Japan: for decades it held an ultra-loose policy and even negative rates, but in 2024 it exited this regime, raising rates for the first time in 17 years. The more the courses of two banks diverge, the wider their currency pair swings. I myself don't guess the meetings, that's a lottery for a forecaster; I wait for the decision and watch what it did to the chart, reading the reaction by volume at a level.

Out of the rate gap grows a mechanic worth naming: the carry trade. If you borrow money in a low-rate currency and hold a high-rate one, the rate difference drips to you as income for merely holding the position, through the swap or rollover. For years this pushes capital one way: the cheap currency is sold, the expensive one is accumulated, and the pair stretches into a trend not because of the chart but because of the funding flow. The Bank of Japan, with its ultra-low rates, was for decades the main funding currency: traders borrowed in yen to put the money into higher-yielding assets. Carry matters most on the unwind: when the funding currency rate suddenly rises, the flow built up over years unwinds sharply and the pair flies back far faster than it climbed. I do not trade the swap itself, but I keep in mind the carry behind a pair to understand where a trend gets its long-burning fuel.

In short: A rate up firms the dollar and pressures risk, down the other way, and a lag of more than six months stretches the trends; the Fed sets the tone for the world, and I don't guess the meeting but follow capital's reaction on the chart.

Global fundamentals: risk-on and risk-off regimes

If you rise above the individual figures, the whole macro picture comes down to one chain. On their own, inflation or GDP affect the market not directly, they affect central banks' rate decisions, and the rate already moves both the currency and the appetite for risk. At the centre of the system stands the dollar: the dollar index is a common yardstick for all currencies, and the moment it weakens, assets priced in it are revalued upward, supporting both the stock market and crypto.

It's handy to keep in mind two regimes the market lives in. When money is plentiful and investors are calm, capital readily goes into stocks, commodities and cryptocurrency, this is the risk-on regime. When there's fear in the market or money is dear, capital runs back into the dollar and protective instruments such as bonds, this is the risk-off regime. Understanding which regime is on now is useful even to a pure technician, so as not to row against the general current. Onto the concrete the world's stock indices this wave projects directly, lifting them in risk-on and pressing them in risk-off. For me this whole picture is the direction of the wind: it tells me whether it's a tailwind for risk assets today or a headwind, but the trade itself I still take off the chart.

In short: Macro hits the market through the rate: dear money firms the dollar and turns on risk-off, cheap money drives capital into stocks, commodities and crypto in a risk-on regime, and at the centre of the system stands the dollar.

The economic calendar: how to use it

An economic calendar is a table of upcoming economic events with the date, time and degree of their importance, where for each event the forecast, the previous value and the actual result are shown. Large releases in it are highlighted in red, smaller ones in yellow or grey. In essence it's a slice of the fundamentals: it suggests which data and at what hour will rock the market.

And straight to the point: for a beginner the calendar is more useful as a shield than as a sword. Its main role is not to let you be caught off guard. You know that in an hour US labour-market data comes out, which means you don't open a calm trade right before it, that's basic caution. Not all news is equal in force. The main event for the currency market is the US non-farm employment report, it comes out on the first Friday of the month and gives powerful volatility on the dollar; alongside it in force are inflation, rate decisions from the Fed and other central banks, and GDP reports. The logic of them all is one: they change participants' expectations, and the market sharply revalues assets. But large capital prepares for them in advance, and often the main move begins even before the figure itself. So I simply mark these dates, and then watch what the market will show through volatility and volume, when the dust has settled.

In short: The calendar is a schedule of news with a forecast and importance; its job is to warn, not to give a signal, so the market is jolted most by the NFP of the first Friday, inflation, Fed rates and GDP.

Why the market reacts to expectations while Smart Money acts ahead

Now begins what the whole conversation is for, and here my approach kicks in. The market feeds not on the facts themselves but on the expectations around them. The forecast lands in the price even before the release: futures play out in advance the raised probability of one or another rate step. Large capital, the smart money, positions for these expectations ahead of time, and at the moment of publication reacts instantly. So when the figure hits the feed and retail rushes into the market, the move is often already done.

This is not insider knowledge and not magic, but speed and working with expectations. No one knows the figure ahead of time, but the large player understands the real value and doesn't guess by indicators. By Wyckoff's own account, operators prepare for major changes half a year or a year ahead and build a position in advance, so the crowd is always late: it reacts to the current price and yesterday's news, while the smart money is already in. The result is a paradox: by the time the news reaches the beginner, it's already played out, and they enter exactly where large capital is exiting. Hence the old rule, buy the rumour, sell the news. I do it more simply: I watch whether large capital is taking part, by effort and result in the volume at a key level. Money is being poured in on the way out, volumes grow, price settles, that's the footprint of smart money, and then I join the reaction, not the forecast. Why news on its own doesn't reverse a trend I show clearly on the example of gold in the video: why fundamental analysis doesn't work for traders.

Since large capital enters ahead of time, the logical question is whether this can be seen in data, not only after the fact on the chart. In part it can. Once a week the COT report, Commitment of Traders, comes out: the US regulator publishes how futures positions are distributed across the large categories of participants. It is a rare window into the real positioning of that same smart money, and a public, free one at that. I do not build an entry on it or treat it as a signal, the figures lag by several days, but as background it helps: when large players accumulate a tilt to one side for years it lines up with my volume picture and adds conviction, while sharp positioning extremes often warn of a nearby reversal. I dislike guessing by indicators, but checking my picture against where large capital actually stands I consider fair.

In short: The market lives on expectations, not the fact: large capital, by Wyckoff, prepares half a year to a year ahead, so retail is late, and I enter by the footprint of volume at a level, not by the forecast.

News trading: why it's dangerous and what to do instead

News trading is a style of trading in which a trader tries to earn on a sharp price move at the moment an important economic news release comes out. It sounds like easy money: the report came out, price shot off, you jumped aboard in time and earned. In practice it's exactly here that beginners lose the fastest, because the direction and force of the reaction are almost unpredictable.

At the moment a strong news release comes out the market behaves chaotically and hostilely toward those in a hurry. Price leaps in both directions, the spread sharply widens, and the stop executes at a completely different price because of slippage. Large players use exactly this: they push price through levels, collect stops, draw false breakouts, and then turn the market around. The classic scenario is a double spike: the figure comes out, price flies sharply one way, beginners jump in after it, and a couple of minutes later it goes just as sharply back and knocks them out by their stops. The market punishes not for an error in the forecast but for entering chaos, and more than once I've seen an account burn up in seconds for people who guessed the direction but didn't survive the shake-out.

So my order is simple and proven. Don't open a trade right at the moment the news comes out. If a position is already standing, know about the release in advance and decide whether to hold it or reduce the risk. And the main thing, wait until the dust settles: I don't catch the first candle, but watch how the price reacted to a key level, and only then look for an entry by my own method, by levels and volume. I treat important releases like a storm: a wise sailor doesn't go out into it for fish but waits it out and catches in calm water, when the real current is visible. Fundamentals say why capital might buy, but not when and at what price, while volume shows this right on the chart afterward: a burst at a level, the absorption of opposing orders, a false push beyond a level to gather liquidity. So I keep the background by fundamentals, and the entry I take by volume and the price's reaction, and why exactly volume is the cause of a move I break down in detail in the course section on volume analysis.

In short: Don't enter at the moment of the news, where the spread and the double spike knock out even the right direction; wait until the dust settles, and take the entry by volume and the price's reaction at a level, keeping fundamentals only as a background.

Frequently asked questions

It's the valuation of an asset through the economy, rates and reporting, to understand its fair value. Cheaper than fair value the asset is considered undervalued, more expensive overvalued. For a long-term investor it's a powerful tool, while for a trader it answers the question of why the price moves, but not when to enter.

Central-bank rates, inflation, employment, the trade balance, business activity (PMI), commodity and gold prices, and geopolitics. The rate affects currencies most of all, because it sets the cost of money in the economy.

PMI is a business-activity index built from surveys of purchasing managers. The 50 mark is the watershed: above it the economy is expanding, below it contracting. The indicator is leading, so the market reacts to it more keenly than to the lagging GDP.

A rate hike makes money more expensive, usually strengthens the dollar and pressures stocks and crypto. A cut makes money cheaper, weakens the dollar and supports risk assets and gold. From the decision to the economy's real reaction there's a lag, as a rule more than half a year.

In my experience you shouldn't pile in at the moment of release: the spread widens, price is thrown in both directions, and a double spike collects stops even with the direction correctly guessed. It's wiser to know about releases in advance, wait out the burst and enter on the price's reaction at a level.

Volume analysis. Fundamentals are kept as a background and the direction of the wind, while the entry is taken by volume and the price's reaction at strong levels, where the footprint of large capital is visible. The principle is simple: first see the action on the chart, then enter, rather than guessing the news in advance.

About the Author

Author: Igor Arapov — independent researcher in the psychology of investment decisions and behavioral finance, practising trader since 2013, founder of arapov.trade, author of a trading book series (ORCID: 0009-0003-0430-778X).