The order you choose decides your fill price, your slippage and, quietly, whose side of the market you stand on. Retail clicks market orders and pays for the hurry, while the big money places patient limit orders and lets price come to it. Learn the whole toolkit, from a plain market order to the hidden orders of smart money, and you stop playing blind against someone who sees more than you do.

The topic looks like a dull alphabet, yet the line between a beginner and a professional runs right through it. I noticed a pattern long ago: retail almost always hammers market orders and pays for the rush, while professionals calmly post limit orders and wait for the market to come to their price. Years at the screen made my own choice plain, for patient orders and a stop on every single trade. I have gathered every order type into one walkthrough, from the simple market order to the hidden orders of smart money, so you stop trading blind against someone who sees more than you.

In this article, we'll cover:

- how a market order differs from a limit one, and why you pay for speed in slippage;

- how the stop order and stop-limit work, and why clusters of stops move price;

- how to place a stop-loss by the level, and why the market deliberately knocks it out;

- how big capital hides volume in icebergs and algorithms, and how to read its footprint by volume.

Let's start with the foundation: what an order is and what its basic types are.

What a trading order is and the types that exist

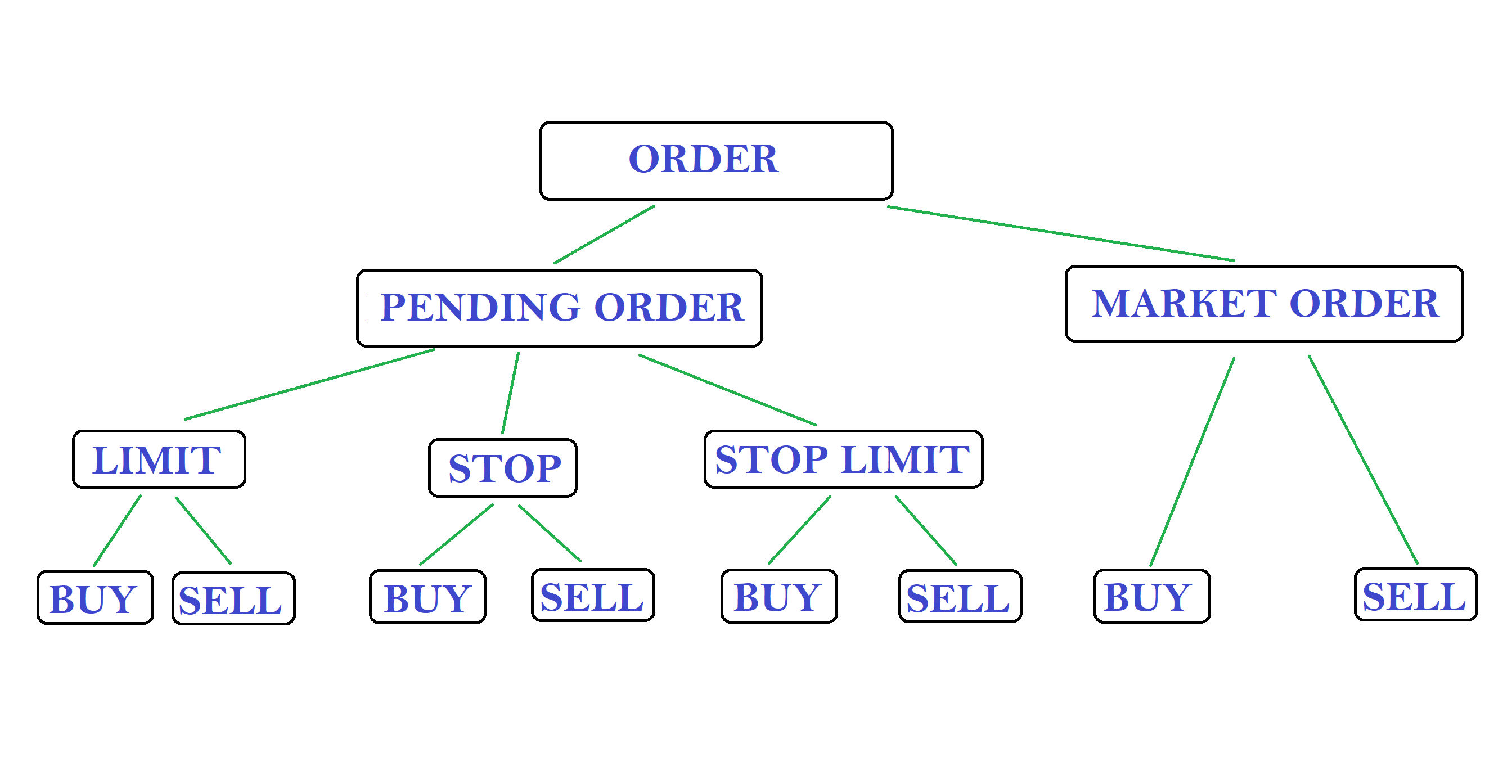

An order is an instruction to the broker to buy or sell an asset under certain rules, and its type directly decides both the price and the speed of the fill. There are several kinds, but it all rests on three pillars.

The first pillar is the market order: it fills immediately at the current price, handing you speed but not control over price. The second is the limit order: it triggers only at your price or better, giving control but no guarantee that price even reaches it. The third is the stop order, a pending command that hangs idle until price gets to a set level, and only then comes alive. Everything else grows from these three: stop-limit, stop-loss, trailing stop, and the hidden orders of big capital. The full map of orders with their triggers I have gathered in the course section on exchange order types, and a visual breakdown of each kind I show in the clip on order types on the exchange: limit, market and stop.

An order has not only a type but also a lifetime, which beginners forget. A day order expires at the end of the trading session if it has not filled. A good-till-cancelled order (GTC) hangs until you remove it yourself or it triggers. There are also strict execution conditions: fill or kill (FOK) demands the whole size be filled at once and in full or cancelled, immediate or cancel (IOC) fills whatever it can right now and drops the rest. Separately there is OCO, one cancels the other: you place two orders together, a take-profit and a stop-loss, and the moment one fires the other is removed automatically. To me this is a working detail of discipline: an OCO pair closes the trade by plan even when I am away from the terminal, and stops a forgotten order from living a life of its own.

In short: An order is a command to the broker on set conditions, and it all rests on three pillars: the market order is speed without price control, the limit order is price control without a fill guarantee, the stop is a sleeping order until its level.

Market order: speed at the cost of slippage

A market order is an instruction to the broker to buy or sell an asset immediately at the best price available at that moment. It is the simplest and most beloved order of beginners, and for that reason the most underrated on risk: behind the harmless buy button hides a fee for haste.

The mechanics go like this. Your order is matched against the opposing ones in the order book, starting from the best price. If your size is larger than what stands on the first level, the order begins to walk the book, taking the next levels at ever worse prices, literally eating liquidity and shifting the quote. That is where slippage comes from, the gap between the price you saw on the screen and the price of the real fill. Do not confuse it with the spread: the spread is the static gap between buy and sell, while slippage is the extra movement your own order causes on top of the spread. It bites hardest in illiquid hours, on thin instruments and at the moment of important news, when liquidity providers scatter. There is a hidden ambush too: the market is watched by algorithms that spot a large market order and move price to meet it, so a big size poured in by one order almost always fills worse than the same size fed in parts. A rough guide on sizing: when your order clearly outweighs what is posted at the best price, a market order will almost surely hand you slippage, and the thinner the market, the wider it runs.

In short: A market order fills instantly, but a large size walks the book and moves price itself, and the fee for speed is the spread plus slippage, which bites hardest on a thin market and on news.

Limit order, and why big money trades with it

The limit order is built as the mirror of the market one: it fills only at your price or better, meaning buy, but no dearer than this mark. You gain control over price, but in exchange you lose the guarantee of a fill, since price may not reach your level at all. That is exactly why exchanges advise beginners to enter with limit orders, so as not to gift money to the market on slippage.

And now an observation that puts a lot in place. Professional participants work mainly with limit orders, while retail hammers market ones. The logic is direct: a market order takes liquidity and moves price against itself, and on a large size that is huge loss a big player cannot afford. So he posts limit orders and waits patiently for the market to come to his price. The result is a paradox that overturned my own approach: the crowd, with its market orders, pours liquidity into the market, while big money, with limit orders, calmly lifts it at a price convenient to itself. This is not advice to you, just a principle borrowed from those who really move the market: I try to enter where I await price, not chase it with a market order. There is a handy hybrid too: place a limit order right at the current price and wait literally a couple of seconds, which is often enough to fill without slippage and lose almost nothing in speed.

In short: A limit order is price control at the cost of an unguaranteed fill; big money enters with limits so as not to push price against itself, and lifts the very liquidity the crowd pours in with its market orders.

Stop order: Buy Stop, Sell Stop and how it moves price

A stop order is a pending order with a set stop price that sleeps until it triggers, and when price touches that level it turns into a market order and fills at the nearest available price. It matters to separate activation from execution here: the stop price only launches the order, while the exact price it fills at is decided by the market at that moment, and on a gap slippage is possible.

It comes in two kinds. A Buy Stop is set above the current price, to enter a buy on a break of resistance upward; a Sell Stop below, to enter a sell on a break of support downward. Here is an example: price stands at 100, resistance above it at 105, you wait for the break and place a Buy Stop just above 105, and if price reaches there you are automatically in the buy, not having missed the move. The trailing stop, which follows price at a set distance, belongs here too. And now the main thing, the reason I count the topic important: stop orders move price. When a cluster of stops triggers, they all turn into market orders at once and spill into the market, pushing price further the same way, sometimes in an avalanche. That is why big capital so loves zones where pending orders stand thick, it is ready fuel for a thrust, and here the effort-and-result pairing works in pure form: the avalanche of market orders becomes the very effort that shoves the quote.

In short: A stop order sleeps until its level and on the touch becomes a market order; a Buy Stop is set above price, a Sell Stop below, and a cluster of stops, when triggered, spills into the market in an avalanche, so stop zones are fuel for a move.

Stop-limit order: price control vs a guaranteed exit

A stop-limit order is a pending order made of two prices: a stop price and a limit price. It works in two steps: first price reaches the stop price, which switches the order on, and then it places not a market but a limit order at your limit price, which will fill only at that price or better.

Here is an example. Say you hold an asset and want out on a fall to 100: you set the stop price at 100 and the limit price at 99. The moment price touches 100, a sell order at 99 or higher appears, but if the market shoots past 99 too fast, the order simply hangs and does not fill. That is the whole difference from an ordinary stop-loss, also called a stop-market: that one becomes a market order on triggering and fills in any case, but at the available price, sometimes with slippage. Put briefly, the stop-market guarantees the exit but not the price, while the stop-limit guarantees the price but not the exit. So the stop-limit fits where price is critical for you and there is no rush: to lock profit on a calm market or to enter on a retest of a level strictly at your mark. But for a protective stop, the one that saves the account, I almost always choose a guaranteed fill, that is, the stop-market. The logic is simple: a stop exists to get you out of a loss, not to get you out gracefully. If in a sharp collapse the stop-limit fails to fill, you stay in a falling position, and that is exactly the trading-without-a-stop we avoid by every means.

In short: A stop-limit is an order of two prices that controls the price but may not fill, while a stop-market fills always at the available price: one guarantees the price, the other the exit, so for protecting the account I take the stop-market.

Stop-loss: how to place it and why every trade needs one

A stop-loss is a protective order that automatically closes a position when price reaches a preset loss level. Its single job is to cap the loss in one trade and not let the market zero the account, and in my firm conviction it must stand on every single trade.

Its value is easiest to see from the opposite side. Most people trade with leverage, which means that if price runs against you far enough, the account zeros on its own, without your part in it. A stop closes the trade earlier, at a loss counted in advance. Beginners drop it not out of laziness but from not knowing where to put it: they slap it down blind, get knocked out, and trust in the tool melts, though the fault lies not with the stop but with the chosen spot. I hide it behind a structural level, under a local low in a buy or above a local high in a sell, adding a small buffer for volatility, since as long as price has not broken that point, the trade's scenario still holds. The second half of the task is the size of the risk: on one trade I set aside no more than a couple of percent of the account, and it is to that sum I fit the size, not the other way round. This is not advice to you, just how I act, since a string of losses is inevitable, and at a risk of a couple of percent it will not kill you, while at ten a few in a row will do. And an entry is worth taking at all only when the possible profit is at least twice the risk. How to count size against risk is laid out in detail in the guide to risk management and capital control.

In short: A stop-loss closes the position itself at a loss counted in advance, and with leverage the account zeros on a sharp move without it; you set it behind a structural level with a buffer and from it size the position at one-to-two-percent risk per trade.

Why the market hunts your stops: the mechanics of stop hunting

A picture familiar to many: you just placed a stop, it was swept at once, and price went exactly where you thought it would. This is not paranoia and not chance. Big money knows perfectly where the crowd stacks its stops, and it stacks them in the most readable spots: snug under a round number and right behind an eye-catching level. That is where liquidity gathers, and at times the quote is deliberately driven into the zone.

In the language of volume analysis this is a shakeout, also called a false break. Price is briefly led past the level, the crowd's stops are knocked out, that liquidity is collected, and price is turned back, leaving those who were swept on the sidelines. In essence a stop left in a predictable spot is a free gift to those with capital and algorithms. Hence the conclusion I repeat constantly: do not give your stop away for free, hide it not on the level itself but behind it, with a buffer, so you are not collected together with the crowd. Volume gives the shakeout away: a weak flow on the break itself plus a fast return of price almost always means a false move. The deeper logic of false break and liquidity collection I lay out in the course section on working with levels and the liquidity deficit.

In short: The market knocks out stops where the crowd holds them, behind a round number and an obvious level: price is led there by a false break on weak volume and turned back, so I hide my stop behind the level with a buffer, not on it.

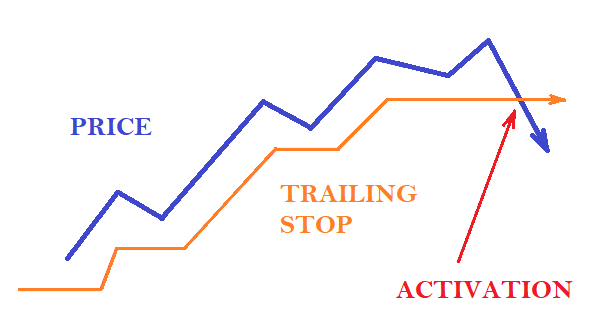

Trailing stop: a moving guard for your profit

A trailing stop is a moving stop-loss that pulls up after price as the trade goes into profit and protects the gain already taken. Unlike an ordinary stop, it does not stand still but trails the market at a set distance.

As soon as the trade is in profit, I pull the stop up after price: in a trend I set it behind each fresh local extreme, gradually locking profit and trimming risk. And here is what you absolutely must not do: move the stop toward the loss in the hope that price will turn, because that breaks the whole plan and almost always ends in a large loss. The rule here is simple and iron: a stop may be moved only toward profit and never toward loss. A stop is set once and then held purely on discipline, as part of the trading plan, not as a variable you feel like nudging just so as not to close in the red.

In short: A trailing stop pulls protection along after price and locks the gain already taken, jumping behind fresh extremes; moving a stop is allowed only into profit and on no account into loss in the hope of a turn.

Iceberg order: how big players hide position size

An iceberg order is a large exchange order that, instead of one big order, is laid out as a run of small ones. At any instant only a small visible share sticks out in the public order book, while the main mass is hidden under the water, hence the name.

The moment the visible portion fills, the next one of the same size steps in to take its place, and so on in a loop until the whole hidden volume has gone into the market. Why a big participant wants this is clear: dump, say, a sell order for a huge oil position all at once, and he presses price down himself, sells worse and sows panic on top. Slicing into an iceberg lets him leave quietly, at a better average, without giving his plan away to the rest. On the chart this is tightly linked to absorption: when opposing volume surfaces again and again at one level and price just cannot break it, someone big is quietly swallowing the flow with a hidden limit order. That level's price then often works as support or resistance. But without romance: to see icebergs live you need access to a level-two order book, the time and sales tape and cluster tools, and most beginners on forex simply do not have that. And on display an iceberg does not say how much volume is still under the water, and not always promises a turn. So I do not chase the iceberg itself in the order book, but read its footprint in volume and in price reaction at the level.

In short: An iceberg is a big order cut into visible slices with the mass hidden; at a level it looks like absorption of the opposing flow, but without L2 and the tape a beginner finds it easier to catch its imprint in volume than the hidden order itself.

Algorithmic orders and spoofing: why I read volume, not the order book

Algorithmic orders are large orders executed by a set algorithm and cut into parts, so a participant can buy or sell a big size without showing the market the real size and intent. The iceberg is only their best-known kind, and the point of all of them is one: to hide the intent.

The logic is direct. Post a huge order whole and it is spotted in the order book at once and price is moved against you, so big money sprinkles size in small portions, picked so they get lost in the ordinary flow. But the order book has a dark side. Spoofing is when a big player posts an imposing order he has no intention of filling, paints fake demand or supply, and then pulls it. That manipulation is outside the law, it draws fines and lawsuits, and it is precisely such tricks that mean the order book cannot be taken at face value. Volume, though, is an honest thing: it shows already-executed trades, and it cannot be faked. So I look not into the order book but at volume at the level. The chief imprint of a big player for me is a spike of volume without a price move, that very effort without result, when pressure is there but price stands, because someone big is eating the whole flow with a hidden limit order. My working order is this: find a strong level, see a spike of volume and a liquidity deficit on it, wait for a false break and slot in behind the big capital with a tight stop. This is not advice to you, just how I act, and the whole beauty is that we, the small participants, need not hide volume: we calmly enter where big capital has already left its tracks.

In short: An algo order slices a big order so big capital gathers size without moving price; the order book can be faked with spoofing, volume cannot, so I look for the big player by a spike of volume without a price move at a strong level.

Orders are a working tool, but they truly come alive only when you see how price forms from the orders in the book and who really steers its movement. The logical next step is to work through how an exchange works as a whole, from the order book and the candle, and to return with that understanding to the choice of order in each particular trade.

Frequently asked questions

A market order fills instantly at any available price: you get speed but pay the spread and possible slippage. A limit order fills only at your price or better and gives control, yet its fill is not guaranteed, since price may never reach it.

It is a pending order that sleeps until its level and on the touch of the stop price turns into a market order. When a cluster of such orders triggers, they all spill into the market at once and push price further the same way, so stop zones serve as fuel for sharp moves.

Not on a round number and not right next to your entry, but behind a structural level with a buffer, where the trade's scenario counts as broken, and from there you size the position at around one to two percent of the account per trade.

A stop-market becomes a market order and always fills, but at the available price, sometimes with slippage. A stop-limit places a limit order and controls the price but may not fill if the market jumps past it. In short: one guarantees the exit, the other the price.

Most often because it sits in an obvious place where the crowd's stops gather, under a round number or right behind a clear level. Liquidity rests there, and price is sometimes pushed into it on purpose with a false break. A stop with a buffer behind the level lowers the chance of that sweep.

An iceberg is a large order cut into visible portions, with only the tip showing in the order book and the main volume hidden. The order book can be faked, while volume records already-executed trades, so big capital is more reliably found by a spike of volume without a price move at a strong level.

About the Author

Author: Igor Arapov — independent researcher in the psychology of investment decisions and behavioral finance, practising trader since 2013, founder of arapov.trade, author of a trading book series (ORCID: 0009-0003-0430-778X).